How to Lower Your Mortgage Payments: Large Bills 411

Your mortgage payment is one of your largest bills. Since it’s one of your largest bills, if you are looking to lower monthly bills, you can look into your mortgage. If you are looking to lower your mortgage payments, there are some things that you can do.

Once you have looked at your budget and have your home picked out there are ways you are able to lower your mortgage payments before you finalize the mortgage.

1. Getting the Lowest Payment Before You Buy the Home

If you want to lower your mortgage payments, the best thing you can do is to work on lowering the payment before you are preapproved and you buy the home. Keep in mind that when you are getting preapproved, you need to factor things in like repairs and maintenance and any upgrades you want to make to the house. The emotional pull of a home can make it easy to rationalize spending more than you feel comfortable with and you don’t want to have buyer’s remorse.

2. Make a Bigger Down Payment

The easiest way to lower your mortgage payments is by borrowing less money. When you make a bigger down payment, you will have a smaller loan. When you have a smaller loan, there will be less that you need to pay back. If you put at least 20% down then you won’t have to pay for any private mortgage insurance. You will be required to have private mortgage insurance if you put less than 20% down. This makes your payments much higher until you reach that threshold of equity in your home.

If you want to make a bigger down payment, there are some things you can do. You can tap into your retirement savings and borrow from your 401k to help boost your down payment. In many cases, the payment is deducted from your pre-tax earnings, and paying this back could be a lot less than the mortgage insurance you have to pay. If you are a first-time homebuyer or haven’t bought a home in the last two years this can be an option for you.

You may also want to consider selling an asset in order to contribute to the down payment. Be sure to keep all the paperwork associated with the sale in order to make the process easier.

If you have family members who have expressed interest in helping you with a home purchase, they are able to contribute money toward your down payment. You need to provide documentation that this is where the money is coming from.

3. Work On Improving Your Credit Score

Your credit score is usually the most important factor when determining the interest rate you will have on your mortgage. The higher your credit score, the lower the mortgage payment. If you are taking out a conventional mortgage then the credit score also plays a role in determining how high your private mortgage insurance premiums are. There are some steps you can take to improve your credit score before you start the house buying process in order to keep your rate and payment as low as possible.

Make sure you make your payments on time. Your payment history has an important impact on your credit score. If you have had any late payments in the last two years, you may want to wait until it’s been a year since the most recent late payments before you apply. If you have trouble remembering payments then set your accounts on auto-pay. Be sure your name is removed from any co-signed accounts with family members that have trouble with on-time payments.

The lower your balance on your card, the better your score will be so keep your balance as low as possible and pay off any debt. Ask your loan officer about a credit rescore. If you recently paid off some credit card debt then you may have had a high balance at the time the report was run. This could have a temporary negative effect on your credit that could be fixed. It usually takes about 30 to 60 days for your credit score to be fixed after you make payment.

4. Reduce Your Mortgage Insurance

If you do have to get mortgage insurance, keep in mind there are different ways you can pay for it besides just including it in your monthly payment. If the seller is paying the closing costs, you may be able to have the seller buy out the mortgage insurance in one lump sum. There are also some other options. You can pay the whole premium at closing so you don’t have to include it in your monthly mortgage payment.

You can also pay the premium upfront in order to get a lower monthly insurance rate. This can be an option if you don’t already have the resources to pay for the whole mortgage insurance premium. This method involves paying a lump sum toward the premium so you get lower payments every month.

5. Consider an Adjustable-Rate Mortgage

Many prefer a 30-year mortgage because it’s stable. However, lenders also have adjustable-rate mortgages, known as ARMs. These provide a lower interest rate and thus a lower monthly period for a set time period. The standard periods are three, five, or seven years and you choose depending on how long you need the lower payment.

However, these lower payments are only temporary. You want to make sure you understand how the loan adjusts after the initial fixed-rate interest period. Adjustable rates are adjustable and are tied to how the market is doing. There are limits on how much the payment can increase after the fixed-rate period but you need to make sure this is the best option for you.

In other cases, an interest-only mortgage may be right for you. With a traditional mortgage, your payment each month goes toward paying down some of the balance and to the interest. As time goes on, you finally start to pay more principal than interest until you pay off the loan. There is a mortgage option that gives you the opportunity to just pay for the interest and no principal. During this period, the payment is much lower since you are only paying the interest and not the principal.

Speak with your loan officer about what happens to the loan balance and your payments after the interest period is over. The loan balance does not go down and you aren’t paying back the loan during this period. After this period ends, you have to pay the entire balance according to the loan terms. For example, if you take out this type of mortgage with a 10-year interest-only period, but the entire loan term is 30 years, then you only have 20 years to pay off the remaining balance and your payments will go up significantly.

No More Worrying about Your Finances

Credit, Debt, Savings etc. - All in One Place

Ways To Lower Your Mortgage Payments After You Already Have the Loan

If you currently have a mortgage, there are still different ways you can lower your mortgage payments depending on your financial situation.

Refinance to a Longer Term

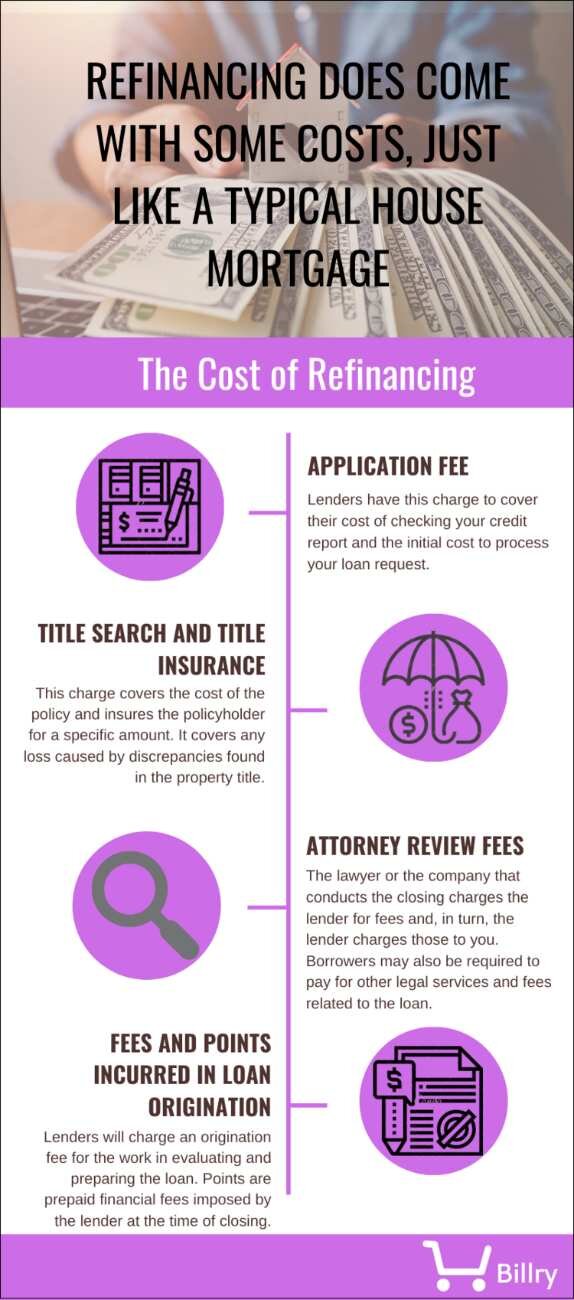

Refinancing your mortgage can help you gain more time to repay and is a popular option when it comes to lowering your mortgage payments. Even though it lowers your mortgage payments, extending the loan term means that you will have extra interest charges, especially if you are going to be paying for a significant amount of time. This may be a last-resort option to lower your mortgage payments. Refinancing your mortgage will depend on what type of loan you originally have.

Conventional Loan: If you have a conventional loan, this is the most common type of refinancing and it’s an easy way to lower payments.

FHA: If you have had your current FHA loan for seven months and have made payments on time then you could be eligible for an FHA streamline refinance. With this, you don’t need to provide any income documentation and only need to verify that there are enough assets for the closing costs. This streamlined process doesn't require an appraisal and can be done quickly without the need for a lot of documentation. If you are saving enough for it to make sense to refinance then this can be a good option.

VA Loans: Similar to FHA, if you have a VA loan there is the VA interest rate reduction refinance loan. Payments have to be on time and you need to break even on closing costs within 26 months in order to be eligible. This break-even time requirement is unique to this. There isn’t an appraisal that is required and employment and income just need to be stated and not verified. Just like with an FHA loan, you only need to make sure you have enough funds to cover closing costs.

USDA Loans: This loan program is for low - to moderate-income borrowers who are within certain eligible rural areas in the country. Just like the other government programs already discussed, the USDA offers a streamlined refinance program. There isn’t a need for credit review or income verification and you don’t need to have new appraisals. The lender needs to verify that you made your payments on time during the last year and that your savings from refinancing reach at least $50 a month.

Refinance the Loan to a Lower Rate

You likely have considered refinancing your loan to a lower rate. Replacing the mortgage with a new loan at a lower interest rate reduces the monthly payment. However, this can be harder than it sounds. You need equity in your property in order to lower your mortgage payments. Rising home values could work in your favor but good credit is also important. A small interest rate improvement may not make enough of a difference when you consider the cost of a refinance. There are closing costs just when you closed your original mortgage so it’s important to run the numbers. Your options for refinancing to a longer term also apply for a lower rate.

Apply for a Possible Loan Modification

If you have a financial hardship and the mortgage payment isn’t affordable, a loan modification may be an option.

A loan modification is when the lender restructures the loan in a way to lower the monthly payment.

You don’t have to already be in default to request a loan modification from the lender. If you are facing a reduction in your income, such as from retirement or a job loss, it’s a good idea to start to get ahead of the issue.

When you reach out to your lender, you may be referred to an approved housing counselor. A loan modification may come at the expense of a note on your credit report that you didn’t pay. You may not even be eligible for a loan modification unless you have missed some mortgage payments. Even if you haven’t missed any payments and are just struggling, it’s always a good idea to stay in communication with your lender so that you don’t risk a foreclosure.

Request a Recast of the Loan

You can also use the option of mortgage recasting. You need to pay at least $5,000 to $10,000 of the current loan balance and then have the lender recast the loan. This can be a good option if you aren’t able to sell your current house before you have to buy a new one and don’t have the resources for a bigger down payment.

Important to note: A recast of your loan isn’t available on government loans so if you have a VA or FHA loan then you need to do a regular refinance.

Eliminate Mortgage Insurance

In order to eliminate mortgage insurance, you need to have more than 20% equity in your home. This means a lender appraisal is needed to show an increase in the home’s market price, depending on how much you originally put down.

In order to get rid of PMI, the first step is to just keep making payments. Keep making payments on your current mortgage until you get to 78% of the original balance. You won’t have to do anything at this point with certain mortgages because federal law requires the mortgage insurance to be removed once you hit this point.

The other option is to have the lender require that it be removed when your house has gone up in value, giving you 20% of your equity. With this option, you may have to pay for an appraisal but it can be worth the money, especially if your PMI is increasing your mortgage payment by a significant amount.

Dispute Property Taxes

If you have an escrow account with your mortgage then your property taxes are likely taking up a huge chunk of your mortgage payment. Property taxes are based on the county’s tax assessment of how much the land or home is worth. Some homes in urban areas are overvalued so the taxes are too high. The assessment is different than an appraisal since it’s only conducted for tax purposes by the county. As a homeowner, you are able to request to have an assessment done again or file an appeal.

Common reasons for appeal include errors in zoning, amenities, or square footage.

You may need to work with a tax attorney for the appeal and to determine whether or not this is worth your effort and if it will help lower your mortgage payments by a significant amount. There can also be property tax exemptions in your area if you are disabled or a senior citizen.

Get New Homeowner's insurance

The other part of your escrow account may be the premium for your homeowner's insurance. This may not be something you check very often but it’s something to consider. It can be subject to sudden increases and it's not uncommon to see your premium increase from year to year. With so many different homeowner’s insurance companies that want your business, it could be time to shop around to see if you can get a lower rate. You may even want to consider doing this even if your premium hasn’t gone up since there could still be a lower rate out there. Learning how to reduce bills is an important skill to have, especially when it comes to insurance.

Rent Out Part of the Home

If you have a part of your home that is unused then having a renter can help you lower your mortgage payments. Even if it’s just a little bit, it can still make a difference to help you offset the monthly mortgage payment, especially if the payment is beginning to feel like too much or there are other unexpected expenses that pop up.

Conclusion

There are plenty of different ways to lower your mortgage payments and it can start before you even buy the home. When shopping for a new home, keep your budget in mind and don’t let the emotions of buying a new home dictate your decisions. Before you close on a new home, consider your down payment and make it as large as possible to avoid paying PMI. If you are already in your home then you can refinance your mortgage, figure out how to lower your PMI, or look into a loan modification. Consider your escrow account, your property taxes, and your homeowner's insurance costs.